Credit Card Cashback Rewards 2025 USA: Maximize Your Savings

With inflation continuing to impact household budgets in 2025, smart Americans are turning to credit card cashback rewards to stretch their dollars further. The right cash back credit cards can put hundreds of dollars back in your pocket annually, making every purchase work harder for your financial goals.

Whether you’re shopping at Walmart, filling up at the gas station, or paying your monthly utility bills, the best cash back credit cards of 2025 offer unprecedented earning potential. Let’s dive into how you can maximize your rewards and build a smarter spending strategy.

Table of Contents

What Are Credit Card Cashback Rewards and Why They Matter in 2025

Credit card cashback rewards are percentage-based rebates you earn on purchases made with your credit card. Unlike points or miles that require complex redemptions, cash back is straightforward – you literally get money back.

As of 2025, the average cash back rate on credit cards is 1.17% cash back on qualifying purchases, according to WalletHub’s latest Credit Card Landscape Report. However, the best cards significantly exceed this average.

Why Cash Back Matters More Than Ever

With consumer prices still elevated from recent inflationary pressures, every percentage point of cash back represents real savings. The U.S. economy could remain resilient into 2025, with continued growth, but households are increasingly strategic about maximizing their purchasing power.

Smart savers understand that cash back on credit card purchases essentially provides an instant discount on everything they buy – from groceries to gas to online shopping.

Types of Cash Back Credit Cards: Finding Your Perfect Match

Flat-Rate Cash Back Cards

Flat-rate cards generally offer 1% to 2% for all purchases, although you may find a card promotion for a higher rate. These cards with cash back are perfect if you want simplicity without category restrictions.

Best for: Busy professionals, frequent travelers, anyone wanting “set it and forget it” rewards.

Category Rotating Cards

These credit cards for cash back offer higher percentages (typically 5%) on rotating categories that change quarterly. Common categories include:

- Grocery stores and supermarkets

- Gas stations and automotive

- Restaurants and dining

- Online shopping and e-commerce

- Department stores

Best for: Organized spenders who can track quarterly categories and activate bonuses.

Tiered Cash Back Cards

These cash reward credit cards offer different percentages for different spending categories year-round. For example:

- 3% on dining and drugstores

- 2% on grocery stores and gas stations

- 1% on all other purchases

Best for: Families with predictable spending patterns in specific categories.

Top Credit Card Cashback Rewards Strategies for 2025

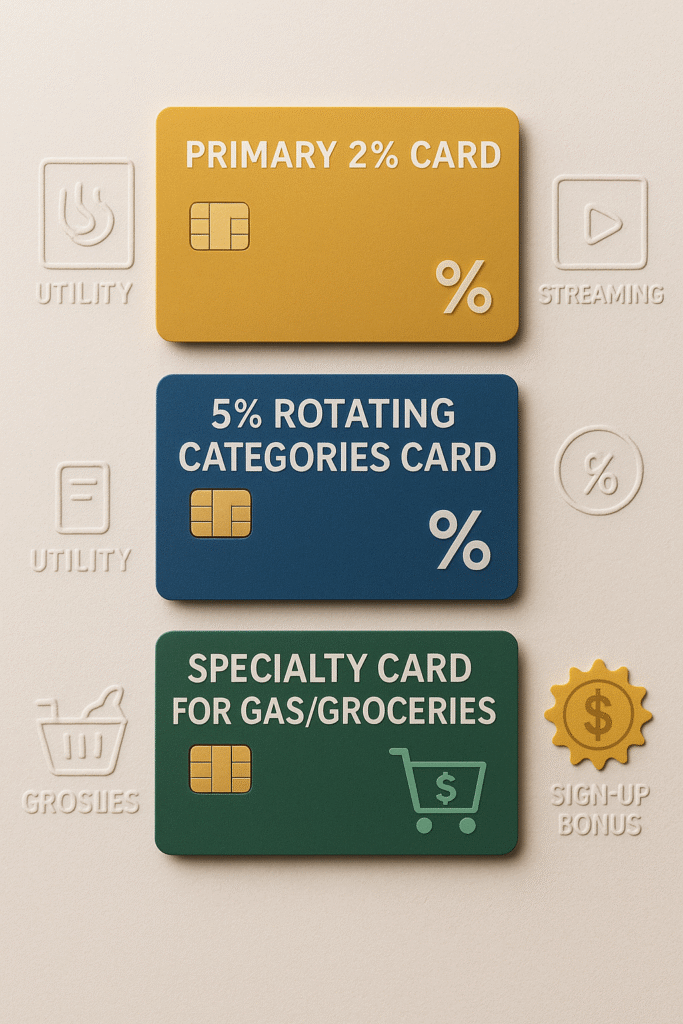

Strategy 1: The Multi-Card Approach

Smart cardholders use multiple cash back cards to maximize rewards across all spending categories:

- Primary Card: Flat-rate 2% card for most purchases

- Category Card: 5% rotating categories card

- Specialty Card: High-rate card for your biggest expense (gas, groceries, etc.)

Strategy 2: The Sign-Up Bonus Focus

The average initial bonus is $229 cash back. Target cards offering substantial welcome bonuses:

- Chase Freedom Unlimited: Often $200 after spending $500

- Capital One Quicksilver: Frequently $200 after spending requirements

- Discover it Cash Back: 100% cash back match in your first year

Strategy 3: The Everyday Essentials Optimization

Focus your credit cards with cash back on unavoidable expenses:

- Utility bills (electric, water, internet)

- Insurance payments (auto, home, health)

- Subscription services (Netflix, Spotify, gym memberships)

- Grocery shopping at stores like Walmart, Target, Costco

Maximizing Your 2025 Cash Back Earnings: Advanced Tips

Tip 1: Understand Spending Caps

Many cash back cc options have quarterly or annual caps on bonus categories. Track your spending to maximize high-rate earnings before hitting limits.

Tip 2: Time Large Purchases Strategically

Plan major expenses around sign-up bonuses and favorable categories. Buying appliances during a “home improvement” quarter can dramatically boost your cash back credit earnings.

Tip 3: Pay Balances in Full Always

Interest charges eliminate cash back benefits. Many cards offer 0% Intro APR for 15 months from account opening on purchases and balance transfers, providing breathing room for large purchases.

Tip 4: Stack with Store Programs

Combine cash back on credit card rewards with:

- Store loyalty programs (Target RedCard savings + credit card cash back)

- Shopping portals (earning cash back through credit card + portal)

- Manufacturer coupons and rebates

Best Credit Card Categories for Maximum Cash Back in 2025

Grocery Stores: The Household Essential

With food costs remaining elevated, grocery cash back provides significant savings. Target stores like:

- Walmart Supercenters

- Kroger and affiliates

- Safeway locations

- Local grocery chains

Gas Stations: Fuel Your Savings

Transportation costs consume a major portion of household budgets. Focus on:

- Shell, Exxon, BP stations

- Costco gas (often cheapest + cash back)

- Local gas station chains

Dining and Restaurants: Eating Out Rewards

As Americans continue dining out post-pandemic, restaurant cash back matters:

- Fast food chains (McDonald’s, Subway, Chick-fil-A)

- Casual dining (Applebee’s, Olive Garden)

- Local restaurants and coffee shops

Online Shopping: E-commerce Cash Back

With online shopping continuing to grow, maximize digital purchases:

- Amazon (often highest category rates)

- Target.com, Walmart.com

- Specialty retailer websites

How Interest Rates and Economic Trends Impact Cash Back in 2025

The Federal Reserve’s monetary policy significantly affects credit card cashback rewards programs. Labor markets have softened but remain resilient, with unemployment at 4.2 percent, up from 3.7 percent at the start of 2024.

Higher interest rates mean:

- Credit card companies can afford more generous rewards

- Consumers must be more careful about carrying balances

- The value of immediate cash back increases relative to delayed gratification

Understanding these economic factors helps you make smarter decisions about which cash back credit cards to prioritize. For more insights on how rate changes affect your finances, check out our analysis at https://smartsaveusa.com/fed-raises-rates-2025-savers-guide/.

Common Cash Back Mistakes to Avoid in 2025

Mistake 1: Chasing Categories You Don’t Use

Don’t choose a dining-focused cash reward credit card if you rarely eat out. Match cards to your actual spending patterns.

Mistake 2: Ignoring Annual Fees vs. Earnings

Calculate whether annual fees exceed your expected cash back earnings. Many no-fee cards provide better net value.

Mistake 3: Missing Activation Requirements

Many quarterly category cards require activation. Set calendar reminders to enable bonus categories.

Mistake 4: Letting Cash Back Expire

Some programs have expiration dates or minimum redemption amounts. Redeem regularly to avoid losing earned rewards.

Comparing Cash Back vs. Other Rewards in 2025

Cash Back vs. Travel Points

Cash back credit provides immediate, flexible value while travel rewards offer potentially higher redemption rates for those who travel frequently.

Cash back advantages:

- No blackout dates or restrictions

- Instant value recognition

- Protection against devaluation

- Simpler redemption process

For investment-minded individuals considering broader financial strategies, explore our comparison of https://smartsaveusa.com/etfs-vs-mutual-funds/ to understand how cash back earnings can fund your investment goals.

Cash Back vs. Store Credit Cards

Store-specific cards with cash back often offer higher rates at particular retailers but limit flexibility. Consider:

- Amazon Prime Rewards Visa: 5% back at Amazon, 2% at gas stations/restaurants

- Target RedCard: 5% off all Target purchases

- Costco Anywhere Visa: 4% on gas, 3% on restaurants and travel

Building Your 2025 Cash Back Strategy

Step 1: Analyze Your Spending

Review three months of expenses to identify your top categories:

- Fixed expenses (utilities, insurance, subscriptions)

- Variable expenses (groceries, gas, dining)

- Occasional expenses (travel, home improvement, electronics)

Step 2: Choose Your Card Portfolio

Select 2-3 cash back credit cards that complement each other:

- One flat-rate card for general spending

- One category-specific card for your highest expense

- Optionally, one rotating category card for quarterly bonuses

Step 3: Set Up Automatic Systems

- Enable automatic bonus category activation

- Set up automatic full balance payments

- Schedule monthly cash back redemptions

Step 4: Track and Optimize

Monitor earnings quarterly and adjust your strategy based on:

- Spending pattern changes

- New card offerings

- Category calendar updates

Bank-Specific Cash Back Programs Worth Considering

Chase Freedom Series

Chase offers multiple credit cards with cash back options:

- Freedom Unlimited: Flat 1.5% on everything

- Freedom Flex: 5% rotating categories + 3% on dining/drugstores

- Combined earning potential: Up to 6.5% on optimized spending

Capital One Quicksilver

Unlimited 1.5% cash back on all purchases with no category restrictions or caps.

Discover it Cash Back

Unique 100% cash back match in your first year, effectively doubling all earnings. 5% rotating categories plus 1% on everything else.

Maximizing Cash Back at Major US Retailers

Walmart Strategy

- Use a 2% flat-rate card for general Walmart purchases

- During grocery quarters, use 5% category card for Walmart Grocery pickup

- Stack with Walmart+ membership for additional savings

Costco Optimization

- Costco Anywhere Visa: 4% on gas, 3% on restaurants/travel, 2% at Costco

- Time major purchases during favorable categories

- Combine with Costco Executive membership 2% rebate

Amazon Approach

- Amazon Prime Rewards Visa: 5% back at Amazon

- Stack with Amazon Prime benefits

- Use for Subscribe & Save orders to maximize both convenience and rewards

2025 Economic Factors Affecting Your Cash Back Strategy

Inflation Impact on Rewards Value

Higher prices would likely slow consumer spending, with higher prices eroding the real purchasing power of consumers. This makes cash back on credit card purchases even more valuable as immediate relief.

Interest Rate Environment

Current rate trends affect both:

- Credit card APRs (making balance payoffs more urgent)

- Savings account rates (affecting cash back investment potential)

For banking strategies that complement your cash back approach, consider opportunities like those detailed in our https://smartsaveusa.com/wells-fargo-325-checking-bonus/ guide.

Consumer Spending Patterns

Credit card data shows consumer spending has remained resilient, indicating continued opportunities for cash reward credit cards to provide meaningful savings.

Tax Implications of Cash Back Rewards

Cash back earned through normal spending is generally not taxable income. However:

- Sign-up bonuses over $600 may trigger 1099 forms

- Business card rewards have different rules

- Cash back from referrals might be taxable

Consult tax professionals for specific situations involving substantial reward earnings.

Technology and Cash Back: Mobile Apps and Tools

Essential Apps for 2025

- Issuer Apps: Real-time spending tracking and category activation

- Mint/YNAB: Budget tracking with reward optimization

- Rakuten: Additional cash back through shopping portals

- Honey: Automatic coupon application plus card recommendations

Automation Features to Enable

- Automatic category enrollment for rotating cards

- Balance alerts to prevent interest charges

- Spending notifications to track progress toward caps

- Automatic cash back redemptions

Advanced Cash Back Tactics for 2025

Manufactured Spending (Legal Methods)

- Gift card purchases during favorable categories (where permitted)

- Prepaid cards for bill payments

- Money order strategies (bank-dependent)

Warning: Only pursue strategies explicitly allowed by card terms. Violations can result in account closure.

Business vs. Personal Card Strategy

Business cash back cc options often provide:

- Higher category limits

- Different bonus categories

- Enhanced sign-up bonuses

- Expense tracking features

Consider business cards if you have legitimate business expenses or side income.

FAQs A Credit Card Cashback Rewards

Q1. How do credit card cashback rewards work?

Credit card cashback rewards give you a percentage of your spending back as cash. For example, if you have a 2% cashback card and spend $1,000, you’ll earn $20 back. Some cards offer flat-rate cashback, while others give higher rates in specific categories like groceries, gas, or dining.

Q2. Which credit card gives the highest cashback in the USA?

The best cashback cards in 2025 include:

Citi Double Cash: Up to 2% on all purchases

Blue Cash Preferred® Card: 6% on groceries, 3% on gas

Chase Freedom Flex: 5% on rotating quarterly categories

Your ideal card depends on your spending habits—if you spend heavily on groceries, a category card might be better; for simplicity, a flat-rate card is best.

Q3. Is cashback better than travel rewards or points?

Cashback is better if you want simple, flexible savings that can be used for anything bills, groceries, or even investments. Travel rewards often offer higher value for flights or hotels but require more effort for redemption.

Q4. Do cashback rewards ever expire?

For most major U.S. credit card issuers, cashback rewards don’t expire as long as your account remains open and in good standing. However, some cards have redemption minimums or expiration policies, so always check your card terms.

Q5. How much cashback can I realistically earn per year?

The average U.S. household spending $50,000 annually can earn between $500–$1,500 a year with the right combination of cards and strategies like rotating categories, sign-up bonuses, and stacking rewards with store loyalty programs.

Regional Considerations for US Cash Back Users

West Coast Strategies

Focus on categories relevant to higher cost-of-living areas:

- Enhanced grocery rewards for expensive markets

- Gas cash back for longer commutes

- Restaurant rewards for dining-heavy cultures

Midwest Optimization

Emphasize practical categories:

- Home improvement and hardware stores

- Grocery and bulk shopping (Costco, Sam’s Club)

- Gas station rewards for rural driving

Northeast Approaches

Target urban spending patterns:

- Public transportation and ride-sharing

- Higher-end grocery stores

- Restaurant and entertainment venues

Southeast Planning

Consider regional retail preferences:

- Walmart and regional grocery chains

- Gas stations and convenience stores

- Home improvement for year-round projects

The Future of Cash Back: 2025 Trends and Predictions

Emerging Categories

Credit card companies are adding new bonus categories reflecting changing consumer habits:

- Electric vehicle charging stations

- Streaming services and digital subscriptions

- Health and wellness spending

- Home delivery services

Technology Integration

Expect enhanced features in 2025:

- AI-powered spending optimization

- Real-time cash back notifications

- Automatic category switching

- Enhanced fraud protection

Competitive Landscape

Cash back credit cards continue evolving with:

- Higher standard rates (approaching 2% flat-rate as new normal)

- More flexible category definitions

- Enhanced mobile app experiences

- Integration with budgeting and financial planning tools

External Resources for Cash Back Research

For official guidance on credit card regulations and consumer protections, visit the Consumer Financial Protection Bureau website.

The Federal Trade Commission provides important information about credit card marketing and terms disclosure requirements.

Building Long-Term Wealth with Cash Back Earnings

Investment Strategy

Instead of spending cash back immediately, consider:

- Directing earnings to emergency funds

- Funding retirement accounts (IRA contributions)

- Building investment portfolios

- Paying down high-interest debt

Compound Growth Potential

$500 annual cash back invested at 7% returns grows to over $7,000 in 10 years. Your credit card cashback rewards can become a significant wealth-building tool when invested wisely.

Integration with Overall Financial Planning

Cash back earnings should complement broader financial strategies:

- Emergency fund building (aim for 3-6 months expenses)

- Debt elimination (starting with highest interest rates)

- Retirement savings acceleration

- Investment account funding

Red Flags: When Cash Back Cards Don’t Make Sense

High Interest Rate Risk

If you carry balances, interest charges eliminate cash back benefits. Interest rates range from 19.24% to 29.24% variable APR on many cards, far exceeding cash back earnings.

Annual Fee Calculations

Cards with annual fees must generate enough additional cash back to justify the cost. Always calculate net value:

Net Cash Back = Total Earnings – Annual Fee – Interest Charges

Overspending Temptation

Don’t increase spending to earn more cash back. The goal is maximizing rewards on necessary purchases, not creating new expenses.

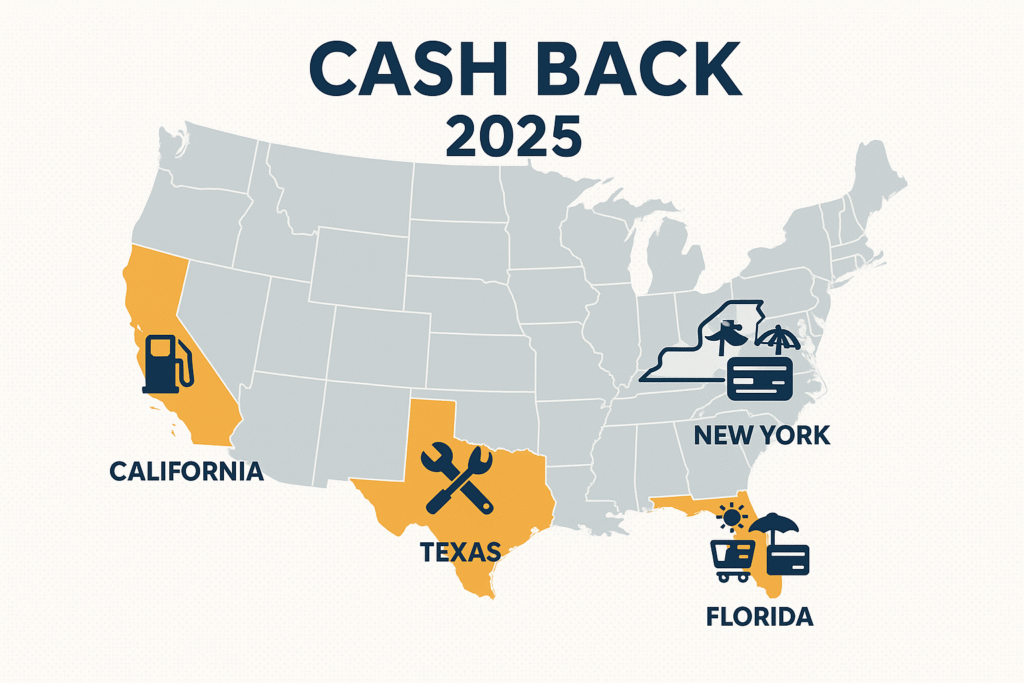

State-Specific Considerations for Cash Back Optimization

California Users

High gas prices make fuel categories especially valuable. Target cards offering 4-5% on gas stations.

Texas Residents

No state income tax means more disposable income for strategic spending. Focus on home improvement and restaurant categories.

New York Shoppers

High cost of living makes every percentage point crucial. Prioritize grocery and transportation categories.

Florida Families

Year-round outdoor activities create opportunities for seasonal category optimization and travel-related cash back.

Credit Score Impact and Cash Back Cards

Building Credit with Cash Back

Cash back credit cards can improve credit scores through:

- Payment history establishment (35% of score)

- Credit utilization management (30% of score)

- Account age building (15% of score)

- Credit mix diversification (10% of score)

Score Requirements by Card Type

- Excellent Credit (740+): Premium rewards cards with highest rates

- Good Credit (670-739): Most standard cash back cards

- Fair Credit (580-669): Secured cards with modest cash back

- Poor Credit (<580): Focus on credit building before rewards optimization

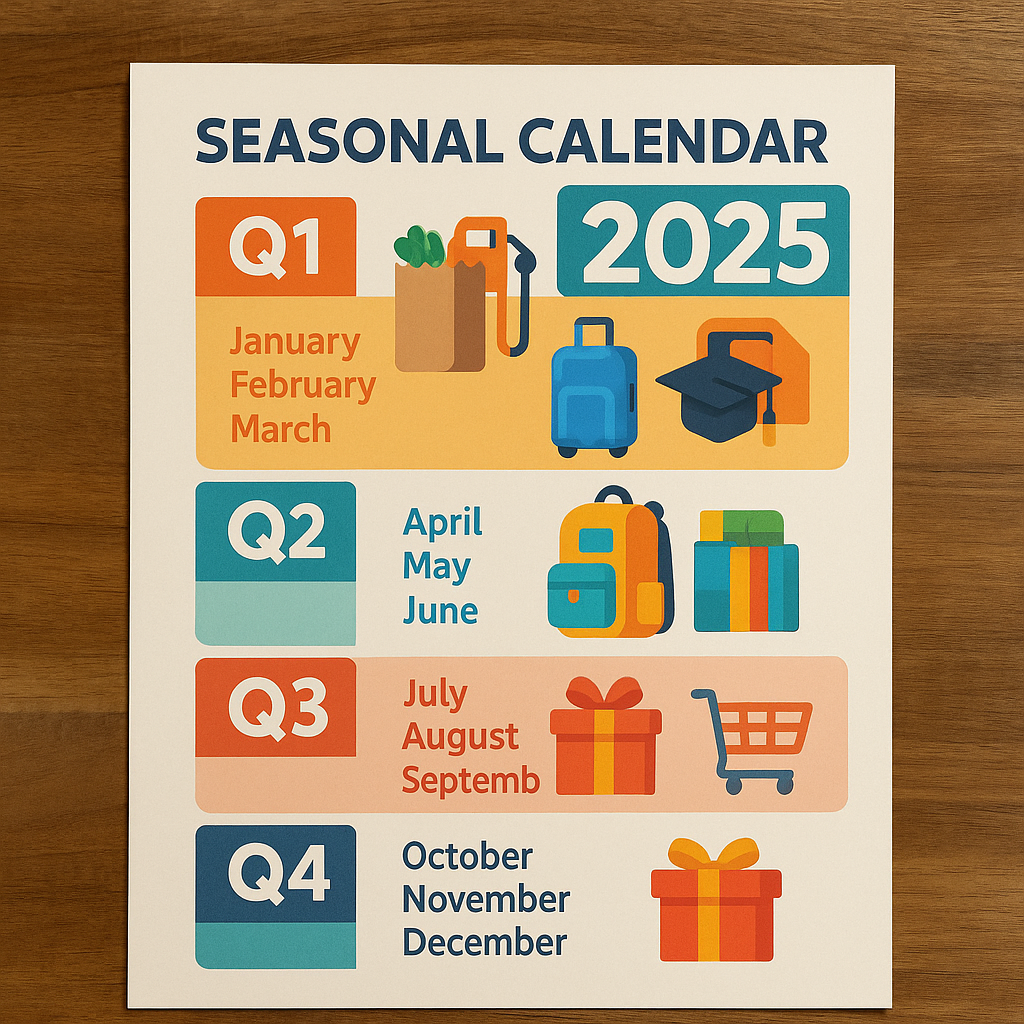

Seasonal Cash Back Optimization Calendar

Q1 (January-March)

- Target grocery and pharmacy categories

- Use tax refunds for sign-up bonus spending requirements

- Plan annual fee card applications

Q2 (April-June)

- Activate gas and travel categories for summer preparation

- Mother’s Day and graduation spending optimization

- Home improvement project planning

Q3 (July-September)

- Back-to-school shopping strategies

- Summer travel and entertainment categories

- Prepare for Q4 holiday spending

Q4 (October-December)

- Holiday shopping category activation

- Online shopping and department store bonuses

- Year-end cash back redemption and tax planning

Conclusion: Start Maximizing Your Credit Card Cashback Rewards Today

The landscape of credit card cashback rewards in 2025 offers unprecedented opportunities for smart savers. With average earnings potential exceeding $500 annually and top strategies reaching $1,500+, the right approach can significantly impact your household budget.

Remember these key principles:

- Match cards to your actual spending patterns

- Always pay balances in full to avoid interest

- Stack multiple strategies for maximum benefit

- Stay informed about category changes and new offerings

Whether you’re dealing with inflation’s continued impact on grocery bills or looking to offset rising gas prices, cash back credit cards provide a practical solution for stretching your budget further.

Ready to transform your spending into savings? Start by analyzing your monthly expenses and identifying which credit cards for cash back align with your lifestyle. Every purchase is an opportunity to earn money back – make sure you’re maximizing every transaction.

Take action today: Visit SmartSaveUSA.com for personalized card recommendations, spending optimization tools, and exclusive strategies to boost your cash back earnings. Your future self will thank you for every dollar saved through smart credit card cashback rewards decisions.