7 Proven Freelancer Budgeting Tips for When Clients Pay Late

Late client payments can wreck even the most carefully planned freelancer budget. If you’re tired of scrambling to cover rent when that $3,000 invoice sits unpaid for weeks, you’re not alone. Smart freelancer budgeting tips can transform your financial stress into steady cash flow management, even when clients drag their feet on payments.

According to the U.S. Bureau of Labor Statistics, over 57 million Americans work as freelancers, and payment delays affect nearly 74% of independent contractors. The good news? With the right budgeting strategies, you can weather these storms and build a thriving freelance business.

Table of Contents

Why Traditional Budgeting Fails Freelancers

Most budgeting advice assumes steady paychecks every two weeks. Freelancers face a different reality: feast-or-famine income cycles, seasonal client demands, and the dreaded late payment epidemic.

Traditional budgeting methods fall short because they don’t account for:

- Irregular income timing

- Client payment delays averaging 30–60 days

- Seasonal business fluctuations

- Emergency business expenses

That’s why freelancer budgeting tips and budgeting tips for freelancers are so important. Instead of using outdated methods, learning how freelancers can budget with proven freelancer budgeting strategies can help create financial stability, even when client payments are unpredictable.

Smart Freelancer Budgeting Tips That Actually Work

1. Build Your Payment Buffer Fund

The foundation of effective freelancer budgeting strategies starts with creating a payment buffer fund—separate from your emergency fund. This buffer helps freelancers cover 2–3 months of essential expenses while waiting for slow-paying clients.

How to build it:

- Save at least 20% of each client payment into a dedicated buffer account.

- Use high-yield savings accounts offering 4.5–5% APY (as of 2025) to grow your buffer faster.

- Target at least 90 days of bare-minimum expenses—about $6,000–$12,000 for most freelancers.

- Real example: Sarah, a graphic designer, built her payment buffer using these budgeting tips for freelancers, ensuring she never stressed about late payments again.

Learning how freelancers can budget using simple steps like this helps turn unpredictable income into a stable financial plan.phic designer from Austin, built a $8,000 buffer by setting aside $400 from each $2,000 project. When her biggest client delayed a $5,000 payment by two months, she continued paying her mortgage and groceries without stress.

2. Master the 50/30/20 Freelancer Rule

Traditional budgeting suggests 50% needs, 30% wants, 20% savings. Freelancers need a modified approach that also considers late pay ment challenges, taxes payment planning, and how to make pay ment schedules more predictable:

- 40% Essential Expenses: Rent, utilities, groceries, insurance

- 30% Business & Buffer: Software subscriptions, equipment, payment buffer for late invoices

- 20% Taxes: Set aside for quarterly taxes payment obligations to avoid last-minute stress

- 10% Personal Goals: Entertainment, dining out, hobbies

This adjustment protects you from the double whammy of irregular income and surprise expenses, helping freelancers make payment decisions smarter while staying on top of taxes and savings.y of late payments and quarterly tax obligations.

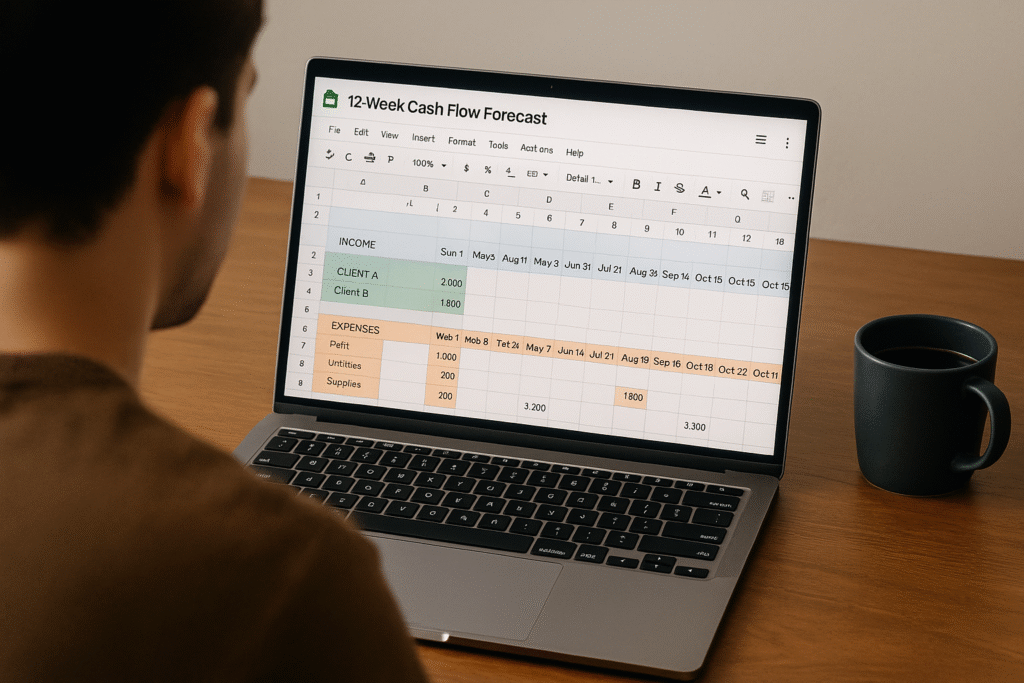

3. Implement Weekly Cash Flow Forecasting

How freelancers can budget effectively requires looking ahead, not just tracking past spending. Create a simple 12-week cash flow forecast showing:

- Expected payment dates for outstanding invoices

- Upcoming business expenses (software renewals, equipment)

- Personal bill due dates

- Estimated tax payment requirements

Pro tip: Use Google Sheets or Excel with conditional formatting to highlight potential cash flow gaps in red.

4. Create Multiple Income Streams

Smart freelancers diversify beyond client work to ensure steady cash flow:

Passive income options:

- Digital products (templates, courses, eBooks)

- Affiliate marketing through your professional blog

- Stock photography or design assets

- Online course platforms like Udemy or Skillshare

Active backup income:

- Retainer clients for predictable monthly revenue

- Part-time remote work (10-15 hours weekly)

- Gig economy platforms during slow periods

Multiple streams reduce your dependence on any single late-paying client.

5. Negotiate Better Payment Terms Upfront

Prevention beats cure when managing freelancer cash flow. Implement these payment strategies:

Contract essentials:

- 50% upfront payment for projects over $1,000

- Net 15 payment terms instead of Net 30

- Late payment fees (2-3% monthly penalty)

- Kill fee clauses for cancelled projects

Payment acceleration tactics:

- Offer 2% discount for payments within 10 days

- Accept credit card payments (even with processing fees)

- Use invoice factoring for large, slow-paying corporate clients

6. Automate Your Tax Payment System

Quarterly taxes can destroy your budget if you’re unprepared. Set up automatic transfers to a dedicated tax account:

Tax automation steps:

- Open a separate high-yield savings account for taxes

- Calculate your effective tax rate (usually 25-30% for freelancers)

- Set up automatic transfers of 25% from each payment

- Make quarterly estimated payments to avoid penalties

2025 update: With inflation impacting tax brackets, freelancers earning over $44,725 should budget 27-30% for federal and state taxes combined.

Advanced Freelancer Budgeting Strategies for 2025

7. Use Technology to Streamline Money Management

Modern freelancer budgeting tips include leveraging fintech tools designed for irregular income:

Essential apps and tools:

- Wave Accounting: Free invoicing and expense tracking

- YNAB (You Need A Budget): Handles irregular income better than Mint

- Cushion: Automatically negotiates bills and finds refunds

- Qapital: Rounds up purchases and saves the change

Banking optimization:

- Use business checking accounts with no monthly fees (Chase Business Complete, Wells Fargo Business Choice)

- Link multiple savings accounts for different goals (taxes, buffer, equipment)

- Set up automatic transfers to remove temptation to spend buffer funds

Smart Investment Strategies for Freelancers

While building your buffer fund, don’t ignore long-term wealth building. As of 2025, freelancers have unique investment opportunities:

Retirement accounts:

- Solo 401(k) allows contributions up to $70,000 annually

- SEP-IRA for simpler setup with lower contribution limits

- Roth IRA for tax-free retirement growth

Investment allocation:

- 80% low-cost index funds (Vanguard Total Stock Market)

- 15% bonds or Treasury I-bonds (currently offering 4.28% in 2025)

- 5% high-risk growth investments

Freelancers looking to grow their savings should also consider investment options carefully. For a detailed guide, check out our ETFs vs Mutual Funds comparison to learn which option works best for your financial goals

Managing Client Relationships to Improve Cash Flow

Communication Strategies That Get You Paid Faster

The best freelancer budgeting tips include managing the people side of your business:

Follow-up sequences:

- Send invoices immediately upon project completion

- Follow up at day 15 with friendly reminder

- Day 30: Professional but firm payment request

- Day 45: Final notice with late fees applied

Client education:

- Explain your payment terms clearly in contracts

- Share the impact of late payments on small businesses

- Offer payment plan options for large invoices

When to Fire Late-Paying Clients

Sometimes the best budgeting strategy is removing problematic clients:

Red flags to watch for:

- Consistently pays after 60+ days despite 15-day terms

- Makes excuses instead of addressing payment delays

- Demands extensive revisions without additional compensation

- Shows disrespect for your time and expertise

Replacement strategy:

- Before firing bad clients, secure 1-2 reliable alternatives

- Focus on industries known for faster payments (tech, healthcare, finance)

- Prioritize long-term retainer relationships over one-off projects

External Linking Suggestions:

- According to the latest data from the U.S. Bureau of Labor Statistics, the number of freelancers in the U.S. continues to rise each year. For tax planning, freelancers should also review IRS quarterly tax information to stay compliant and avoid penalties. Additionally, the Small Business Administration freelancer resources offer valuable guidance on managing a freelance business effectively.

Emergency Financial Planning for Freelancers

Creating Your Freelancer Emergency Action Plan

Beyond basic budgeting tips for freelancers, you need a crisis management strategy:

Three-tier emergency plan:

- Tier 1 (0-30 days): Use payment buffer fund, delay non-essential expenses

- Tier 2 (30-60 days): Activate backup income streams, consider factoring invoices

- Tier 3 (60+ days): Emergency gig work, temporary part-time employment

Insurance considerations:

- Disability insurance for freelancers (policies starting at $50/month)

- Professional liability insurance

- Health insurance through marketplace or spouse’s employer

Building Credit as a Freelancer

Strong credit provides emergency funding options when cash flow turns negative:

Credit building strategies:

- Business credit cards with 0% introductory APR periods

- Personal credit line for smooth cash flow gaps

- Business term loans for equipment or expansion

Recommended business credit cards (2025):

- Chase Ink Business Cash: 5% cashback on office supplies, internet, phone

- Capital One Spark Cash: Flat 2% on all purchases

- American Express Business Gold: 4x points on top spending categories

Freelancers can also take advantage of special bank offers to boost their savings. Don’t miss our guide on the Wells Fargo $325 checking bonus opportunity to learn how you can earn extra cash just for opening an account.

Technology Tools That Simplify Freelancer Money Management

Accounting Software That Works for Irregular Income

How freelancers can budget effectively depends heavily on having the right tracking systems:

Top accounting solutions:

- QuickBooks Self-Employed: Automatic expense categorization, quarterly tax estimates

- FreshBooks: Time tracking integration with invoicing

- Wave: Completely free with optional paid add-ons

Mobile expense tracking:

- Receipt scanning with Expensify or Shoeboxed

- Mileage tracking with MileIQ for client meetings

- Bank account linking for automatic transaction imports

Invoice Management Systems

Getting paid faster starts with professional invoicing:

Key features to look for:

- Automatic payment reminders

- Online payment processing (PayPal, Stripe, Square)

- Read receipts to confirm client received invoices

- Late fee calculations

Industry data: Freelancers using automated invoicing systems get paid 29% faster than those using manual processes, according to 2025 payment industry reports.

Seasonal Budgeting for Freelance Success

Planning for Feast and Famine Cycles

Most freelance businesses experience predictable seasonal patterns. Smart budgeting anticipates these cycles:

Common freelancer seasons:

- Q1 (Jan-Mar): Slow start as businesses reset budgets

- Q2 (Apr-Jun): Steady growth, conference season

- Q3 (Jul-Sep): Summer slowdown, vacation delays

- Q4 (Oct-Dec): Year-end rush, holiday delays

Seasonal strategies:

- Save extra during high-earning quarters

- Schedule non-urgent expenses during lean months

- Plan marketing pushes before predictable slow periods

- Consider seasonal side work during traditional down times

Holiday and Vacation Planning

Unlike traditional employees, freelancers don’t get paid time off. Budget for breaks:

- Calculate lost income for planned vacation days

- Save 1/12th of vacation costs monthly

- Schedule time off between major client deadlines

- Communicate holiday schedules 60 days in advance

Federal rate changes affecting savers

Tax Strategy Integration with Freelancer Budgeting

Quarterly Payment Planning

Missed quarterly taxes can derail your entire budget. Here’s how to stay ahead:

Quarterly tax calendar (2025):

- Q1: Due April 15, 2025

- Q2: Due June 16, 2025

- Q3: Due September 15, 2025

- Q4: Due January 15, 2026

Tax payment strategies:

- Open a dedicated tax savings account with automatic transfers

- Calculate payments based on previous year’s income plus 10%

- Use IRS Form 1040ES for accurate quarterly estimates

- Consider working with a CPA for complex situations

Deduction Tracking That Saves Money

Proper expense tracking can save freelancers thousands in taxes:

Common freelancer deductions:

- Home office expenses (utilities, rent, internet)

- Business equipment and software subscriptions

- Professional development courses and conferences

- Client meeting expenses and travel

Tracking systems:

- Photograph receipts immediately with smartphone apps

- Separate business and personal credit cards completely

- Use accounting software that categorizes expenses automatically

- Keep digital records organized by tax year

Building Long-Term Wealth as a Freelancer

Retirement Planning Without Employer Benefits

Freelancers must create their own retirement safety net:

Retirement account options:

- Solo 401(k): Highest contribution limits for high earners

- SEP-IRA: Simpler setup, good for growing businesses

- Traditional vs. Roth IRA: Consider current vs. future tax rates

2025 contribution limits:

- Solo 401(k): Up to $70,000 ($77,500 if over 50)

- SEP-IRA: 25% of net self-employment income

- Traditional/Roth IRA: $7,000 ($8,000 if over 50)

Health Insurance and Healthcare Costs

Healthcare represents a major expense for freelancers without employer coverage:

Healthcare budgeting essentials:

- Shop marketplace plans during open enrollment (November-December)

- Consider Health Savings Accounts (HSAs) with high-deductible plans

- Budget for dental and vision separately

- Research short-term medical coverage for gaps

Cost-saving strategies:

- Generic prescriptions through Costco or Walmart pharmacies

- Urgent care instead of emergency rooms for non-critical issues

- Telehealth services for routine consultations

- Preventive care to avoid costly treatments later

FAQs How Can Freelancers Budget with Irregular Income?

Q1. How can freelancers budget with irregular income?

Freelancers can use strategies like payment buffer funds, separating business and personal finances, and using budgeting apps designed for variable income to stay on track even when payments are inconsistent.

Q2. What percentage of income should freelancers save for taxes?

Financial experts recommend saving 25–30% of every payment for quarterly taxes. The IRS estimated taxes page offers guidelines for self-employed professionals.

Q3. How can freelancers deal with late client payments?

Use written contracts with clear payment terms, request partial upfront payments, and maintain a 90-day expense buffer to protect against delays.

Q4. What are the best budgeting apps for freelancers?

Popular options include QuickBooks Self-Employed, YNAB (You Need a Budget), and Wave — all designed to handle irregular income and tax planning.

Q5. How much emergency savings should freelancers have?

Freelancers should aim for 3–6 months of living expenses in a high-yield savings account to handle unexpected gaps in income or emergency costs.

Conclusion

Mastering freelancer budgeting tips transforms unpredictable income into financial stability. Start with building a payment buffer fund, implement the modified 50/30/20 rule, and use technology to automate your financial management.

The key to freelance financial success isn’t earning more—it’s managing what you earn smarter. These strategies help you thrive regardless of when clients make payment or how irregular your income becomes.

Ready to take control of your freelance finances? Start saving smarter with SmartSaveUSA.com and discover more money management strategies designed specifically for independent professionals.