Boost Your Credit Score Quickly in 6 Easy Steps

Your credit score is the golden key to financial freedom in America. Whether you’re planning to buy a home, lease a car, or simply qualify for better interest rates, knowing how to boost your credit score can save you thousands of dollars over your lifetime. The good news? You don’t need expensive credit repair services or complicated strategies to see real results.

As of 2025, with the Federal Reserve’s latest rate adjustments continuing to impact borrowing costs, having an excellent credit score is more valuable than ever. The average American credit score sits at 714, but with the right approach, you can join the elite 20% of consumers who maintain scores above 800.

In this comprehensive guide, we’ll walk through six proven steps that can help you boost your credit score quickly and effectively, using strategies that work specifically for US consumers navigating today’s financial landscape.

Table of Contents

Why Your Credit Score Matters More Than Ever in 2025

Before diving into our step-by-step guide, let’s address the elephant in the room: why should you care about your credit score right now?

With inflation still affecting everyday expenses and interest rates remaining elevated compared to previous years, your credit score directly impacts your purchasing power. A difference of just 100 points can mean:

- $50,000+ in savings on a 30-year mortgage

- 3-5% lower interest rates on auto loans

- Access to premium credit cards with cash-back rewards

- Better insurance premiums in most states

- Easier apartment approvals without hefty deposits

Step 1: Check Your Credit Reports for Errors (The 30-Day Quick Win)

The fastest way to improve your credit rating is to identify and dispute errors on your credit reports. According to the Federal Trade Commission, approximately 25% of consumers have errors on at least one credit report that could negatively impact their scores.

How to Get Started:

- Visit AnnualCreditReport.com (the official government-authorized site)

- Download reports from all three bureaus: Experian, Equifax, and TransUnion

- Review every section carefully, including:

- Personal information accuracy

- Account payment histories

- Credit limits and balances

- Accounts that aren’t yours

Real-Life Example:

Sarah from Phoenix discovered a $2,400 credit card debt that wasn’t hers on her Experian report. After disputing it online, her credit score jumped 47 points within 30 days, qualifying her for a better rate on her Wells Fargo auto loan.

Quick Tip: Set a calendar reminder to check your reports every four months, rotating between the three bureaus for year-round monitoring.

Step 2: Pay Down High Credit Card Balances (Target 30% Utilization)

Your credit utilization ratio accounts for 30% of your credit score calculation. This means the amount you owe compared to your credit limits has a massive impact on your ability to boost your credit score.

The 30% Rule Explained:

If your credit limit is $10,000, keep your balance below $3,000. But here’s the insider secret: aiming for under 10% utilization can push your score even higher.

Strategic Payment Timing:

Many Americans don’t realize that credit card companies report balances to credit bureaus on different dates, not necessarily when your bill is due.

Pro Strategy: Make payments twice per month:

- Once mid-cycle to lower your statement balance

- Once before your due date to avoid interest charges

Smart Balance Transfer Approach:

Consider moving high balances to cards with promotional 0% APR offers. Cards like the Citi Simplicity or Chase Slate Edge often provide 15-21 months of interest-free balance transfers for qualified applicants.

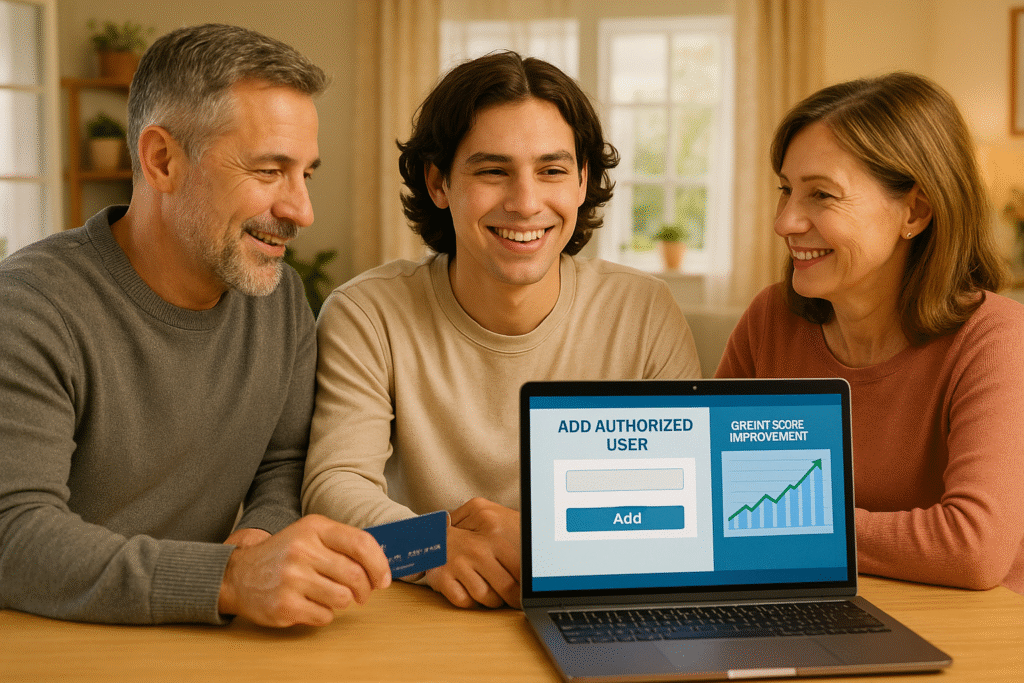

Step 3: Become an Authorized User (The Family Boost Method)

This strategy to improve your credit rating works particularly well for young adults or those rebuilding credit after financial difficulties.

How It Works:

When someone with excellent credit adds you as an authorized user to their account, their positive payment history and low utilization can boost your score within 30-60 days.

Choosing the Right Account:

Ask potential primary cardholders about:

- Payment history: 100% on-time payments for at least 2 years

- Account age: Older accounts provide more benefit

- Utilization: Accounts with low balances relative to limits

Family-Friendly Example:

Miguel’s parents added him as an authorized user on their 12-year-old Costco Anywhere Visa card with a $25,000 limit and 5% utilization. His credit score increased by 78 points over three months, helping him qualify for his first apartment in Denver.

Important Note: Ensure the primary cardholder maintains excellent habits, as negative activity will also affect your credit.

Step 4: Keep Old Accounts Open (Maximize Your Credit Age)

The length of your credit history contributes 15% to your credit score. Many Americans make the mistake of closing old credit cards, unknowingly damaging their credit score improvement efforts.

Why Account Age Matters:

Credit scoring models consider:

- Average account age: Older accounts increase your average

- Oldest account age: Your credit “anchor” shows long-term responsibility

- Total credit history: Longer relationships with lenders build trust

Managing Old Cards Strategically:

- Use them occasionally: Make small purchases every 6 months

- Pay them immediately: Avoid interest charges

- Set up autopay: For recurring bills like Netflix or Spotify

- Monitor for changes: Banks sometimes close inactive accounts

Real-World Impact:

Jennifer from Seattle kept her first credit card (a basic Chase Freedom) open for 15 years, even after qualifying for premium cards. This single account now represents 40% of her credit history length, contributing significantly to her 820 credit score.

Step 5: Diversify Your Credit Mix (But Don’t Go Overboard)

Credit scoring models reward consumers who can manage different types of credit responsibly. Your credit mix accounts for 10% of your score, making it a valuable tool to build credit history. Understanding these percentages and how they’re calculated can help you prioritize your efforts – you can learn more about the specific breakdown at myFICO.com.

Types of Credit That Count:

Revolving Credit:

- Credit cards (Visa, Mastercard, Amex, Discover)

- Home equity lines of credit (HELOCs)

- Store credit cards (Target RedCard, Amazon Prime Card)

Installment Credit:

- Mortgages

- Auto loans

- Personal loans

- Student loans

Smart Diversification Strategy:

Don’t apply for multiple types of credit at once. Instead, gradually add different credit types as you need them naturally.

Example Timeline:

- Year 1: Start with a starter credit card

- Year 2: Add a store card for a major retailer you frequent

- Year 3: Finance a reliable used car

- Year 4+: Consider a mortgage when ready for homeownership

2025 Update on Credit Builder Loans:

Many credit unions now offer “credit builder loans” where you borrow money that’s held in a savings account until you complete payments. These can be excellent for establishing installment credit history.

[Insert related SmartSaveUSA link here]

Step 6: Time Your Applications Strategically (The 14-Day Window Rule)

The final step to boost your credit score involves being strategic about when and how you apply for new credit. New credit inquiries account for 10% of your score, but smart timing can minimize their impact.

Understanding Hard vs. Soft Inquiries:

Hard Inquiries (affect your score):

- Credit card applications

- Mortgage applications

- Auto loan applications

- Personal loan applications

Soft Inquiries (don’t affect your score):

- Checking your own credit

- Pre-approved offers

- Employment credit checks

- Insurance quotes

The 14-Day Shopping Window:

When shopping for mortgages or auto loans, multiple inquiries within 14-45 days (depending on the scoring model) count as a single inquiry. This allows you to compare rates without damaging your credit score improvement efforts.

Strategic Application Timing:

- Space out credit card applications by at least 3-6 months

- Apply for loans when you need them, not “just in case”

- Consider pre-qualification tools that use soft pulls

- Avoid applications during major purchases (like home buying)

Advanced Tips for 2025: What’s Changed This Year

The credit scoring landscape continues evolving. Here are the latest updates that can help you improve your credit rating:

Experian Boost Integration:

Experian now allows you to add utility payments, streaming services, and phone bills to your credit report. This can particularly help consumers with thin credit files.

FICO Score 10T Impact:

The newest FICO model considers trending data, rewarding consumers who show consistent improvement over time. This means your recent positive changes carry more weight.

Buy Now, Pay Later (BNPL) Reporting:

Services like Affirm and Klarna are increasingly reporting payment data to credit bureaus. Make sure to treat these like any other credit obligation.

Common Credit Score Mistakes to Avoid

Even with the best intentions, many Americans sabotage their own credit score improvement efforts. Here are the biggest pitfalls:

Mistake #1: Closing Cards After Paying Them Off

This reduces your available credit and can increase utilization ratios on remaining cards.

Mistake #2: Ignoring Small Balances

A $10 balance that goes to collections can drop your score by 100+ points.

Mistake #3: Co-Signing Without Understanding the Risk

Co-signed accounts appear on your credit report and affect your scores, regardless of who makes payments.

Mistake #4: Assuming All Debt is Bad

Strategic use of credit, paid responsibly, actually improves your creditworthiness.

When to Consider Professional Help

While these six steps can help most consumers boost their credit score, some situations require additional expertise:

- Identity theft recovery

- Complex credit report disputes

- Bankruptcy aftermath planning

- Multiple collection accounts

If you’re dealing with these challenges, consider consulting with a HUD-approved housing counseling agency, which provides free credit counseling services, or review your consumer rights at the Consumer Financial Protection Bureau.

Tracking Your Progress: Free Tools and Resources

Monitoring your credit score improvement doesn’t require expensive monthly subscriptions. Here are reliable free options:

Government Resources:

- AnnualCreditReport.com: Official free credit reports

- Consumer Financial Protection Bureau: Complaint filing and resources

Bank and Credit Union Tools:

- Chase Credit Journey: Free scores for Chase customers

- Bank of America: Free FICO scores for qualifying accounts

- Capital One CreditWise: Free for everyone, not just customers

Credit Card Company Perks:

Many cards now provide free monthly credit scores as a cardholder benefit.

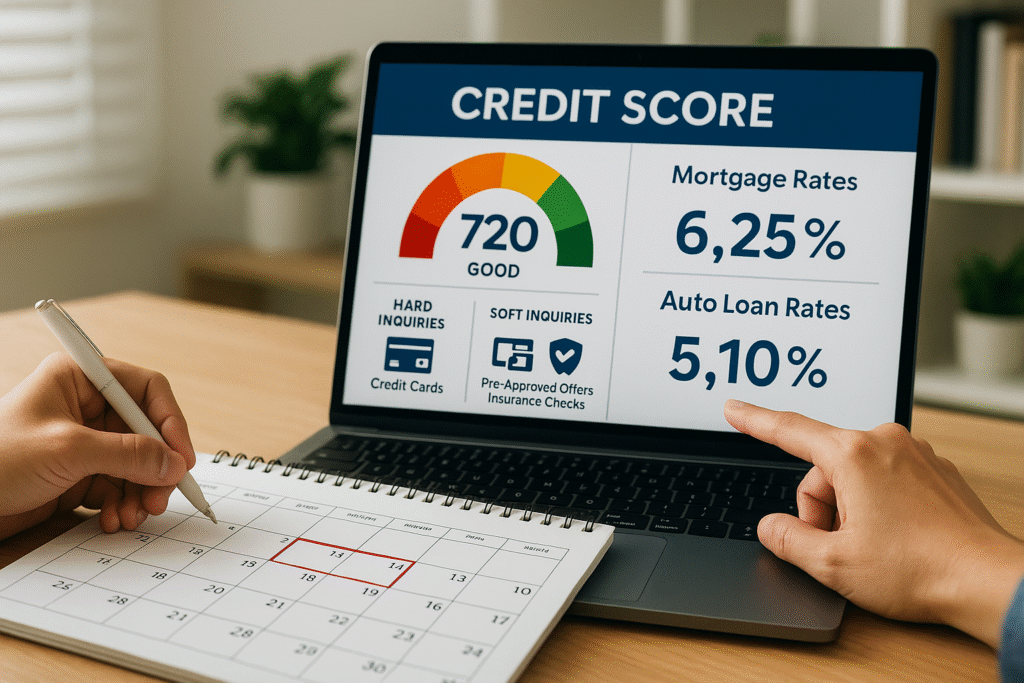

The Financial Impact: Real Numbers for US Consumers

Let’s put the benefits of credit score improvement into perspective with real US market data as of 2025:

Mortgage Savings Example:

- $300,000 home loan, 30-year fixed

- 740+ credit score: 6.5% APR = $1,896 monthly payment

- 640 credit score: 7.8% APR = $2,163 monthly payment

- Monthly savings with higher score: $267

- Total 30-year savings: $96,120

Auto Loan Impact:

- $25,000 car loan, 60-month term

- Excellent credit (750+): 4.5% APR

- Fair credit (650-699): 8.9% APR

- Total interest difference: $2,847

These numbers demonstrate why learning how to boost your credit score isn’t just about financial healthit’s about maximizing your purchasing power.

Frequently Asked Questions

Q1. How quickly can I raise my credit score?

Many people want to know the fastest ways to see credit score improvement—like paying down balances, disputing errors, and becoming an authorized user.

Q2. Will checking my own credit score hurt it?

This is one of the most common concerns. People search whether using free tools like Credit Karma or bank credit monitoring affects their score.

Q3. What’s the ideal credit utilization ratio for the best score?

Americans want clear guidance on whether staying below 30%, 10%, or another percentage impacts their credit the most.

Q4. How many credit cards should I have to build good credit?

People want to know the balance between too few and too many credit cards when trying to build or maintain a strong credit history.

Q5. Can paying off debt improve my credit score instantly?

Many search if paying off a loan, credit card, or collection account will immediately boost their credit rating or if it takes time.

Take Action Today: Your Credit Score Journey Starts Now

Improving your credit score isn’t about quick fixes or expensive services—it’s about understanding how credit works and making consistent, informed decisions. The six steps we’ve outlined can help any American consumer boost their credit score and unlock better financial opportunities.

Remember, credit score improvement is a marathon, not a sprint. Start with the easiest wins: check your credit reports for errors and pay down high balances. Then gradually implement the other strategies as they fit your financial situation.

Your future self will thank you for every point gained. Whether you’re dreaming of homeownership, planning a major purchase, or simply want the financial flexibility that comes with excellent credit, these steps will get you there.

Ready to take control of your financial future? Start saving smarter and building better credit with SmartSaveUSA.com. Check out our related guides on fed raises rates 2025 savers guide, Wells Fargo $325 checking bonus, and ETFs vs mutual funds to maximize your financial growth in 2025.