Credit Score Mistakes That Kill Your Credit

Your credit score determines whether you’ll qualify for that dream home mortgage, get approved for the best credit cards, or even land certain jobs. Yet millions of Americans unknowingly make credit score mistakes that can drop their scores by 100+ points overnight.

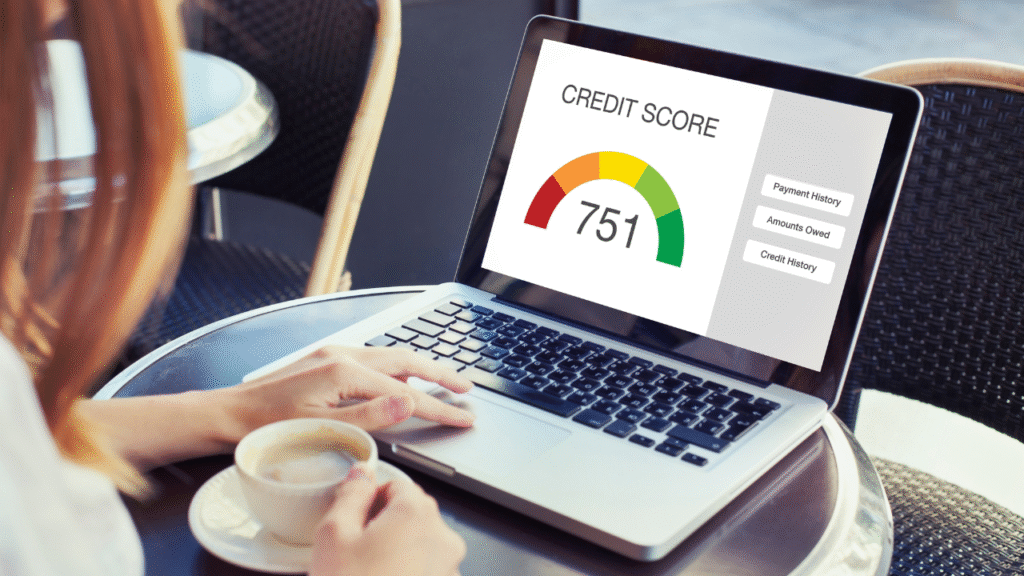

As of 2025, the average American credit score sits at 715, according to recent FICO data. However, simple credit card errors continue to devastate scores across the country, costing consumers thousands in higher interest rates and missed opportunities.

Don’t let these common pitfalls destroy your financial future. Here are the five most damaging credit score mistakes – and exactly how to avoid them.

Table of Contents

Maxing Out Your Credit Cards

Why High Credit Utilization Destroys Your Score

Credit utilization – the percentage of available credit you’re using – accounts for 30% of your credit score calculation. This makes it the second-most important factor after payment history.

Here’s the shocking truth: Using more than 30% of your available credit can significantly hurt your score. But the real damage happens when you max out cards entirely.

Real Example: Sarah from Phoenix had a $5,000 limit Chase Freedom card. When she charged $4,800 for home repairs (96% utilization), her score dropped 45 points in one month.

The 2025 Credit Utilization Strategy

- Keep total utilization below 10% for optimal scores

- Pay balances before statement dates to report lower usage

- Request credit limit increases to automatically lower ratios

- Use multiple cards instead of maxing one card

Pro Tip: Set up balance alerts at 25% utilization. Most banks like Bank of America and Wells Fargo offer free text notifications.

Making Late Payments (Even One Day Late)

How Payment History Impacts 35% of Your Score

Payment history represents the largest chunk of your credit score calculation. A single late payment can remain on your credit report for seven years, making this the costliest of all credit card errors.

2025 Update: Credit card companies have become stricter about reporting late payments. Previously, some issuers offered grace periods, but major banks now report payments late after just one day past the due date.

Late Payment Damage by Score Range

- 740+ Credit Score: Can drop 60-80 points from one 30-day late

- 680-739 Credit Score: Typically drops 60-80 points

- Below 680: May drop 25-45 points (less impact when score already lower)

Action Steps:

- Set up automatic minimum payments for all cards

- Use calendar reminders 5 days before due dates

- Pay twice monthly to stay ahead of due dates

- Consider consolidating due dates to one monthly date

Closing Old Credit Cards

Why Account Age Matters More Than You Think

Closing old credit cards commits two credit score mistakes simultaneously:

- Reduces available credit (increases utilization ratios)

- Shortens credit history length (15% of your score calculation)

Case Study: Mark from Dallas closed his 8-year-old Discover card with a $3,000 limit because he “never used it anymore.” His credit utilization jumped from 15% to 28%, and his average account age dropped by 2 years. Result: 35-point score decrease.

The Smart Way to Handle Unused Cards

Instead of closing old cards:

- Make small purchases once every 6 months

- Set up a recurring subscription (Netflix, Spotify)

- Pay off immediately to maintain activity

- Never close your oldest card unless there’s an annual fee

Exception: Close cards with high annual fees if you’re not using the benefits. But do this strategically – only close one card per year maximum.

Applying for Too Many Cards Too Quickly

How Hard Inquiries Stack Up Against You

Each credit card application triggers a “hard inquiry” that typically drops your score 5-10 points. While one inquiry barely affects your score, multiple applications within months can signal financial desperation to lenders.

The 5/24 Rule Reality: Major issuers like Chase automatically deny applicants who’ve opened 5+ cards in 24 months. This industry standard has tightened considerably since 2024.

Strategic Credit Card Applications in 2025

- Space applications at least 3-6 months apart

- Apply for cards only when you genuinely need them

- Research pre-qualification tools that use soft pulls

- Consider your credit mix before applying

Smart Shopping Window: Credit scoring models typically count multiple inquiries within 14-45 days as a single inquiry when rate shopping for mortgages or auto loans. This doesn’t apply to credit cards.

Federal Trade Commission – Understanding Credit Reports

Ignoring Credit Report Errors

Why 20% of Americans Have Credit Report Mistakes

According to Federal Trade Commission studies, one in five consumers has errors on their credit reports. These credit card errors range from accounts that don’t belong to you to incorrect payment histories.

Common Credit Report Errors:

- Accounts belonging to someone with a similar name

- Closed accounts still showing as open

- Incorrect payment statuses

- Wrong credit limits or balances

- Fraudulent accounts from identity theft

The 2025 Credit Monitoring Game Plan

With three major credit bureaus (Experian, Equifax, TransUnion) and dozens of scoring models, monitoring has become more complex but also more important.

Free Monitoring Strategy:

- Get free reports from AnnualCreditReport.com (official government site)

- Stagger requests – pull one bureau every 4 months

- Use free credit monitoring from credit card companies

- Dispute errors immediately online or via certified mail

Pro Tip: Costco members get free credit monitoring through Costco’s partnership with various credit services. Many employers also offer free credit monitoring as employee benefits.

How to Improve Credit Score After Making These Mistakes

The 90-Day Credit Recovery Plan

Recovery from credit score mistakes takes time, but you can see improvements within 30-90 days:

Month 1:

- Pay all balances below 10% utilization

- Set up automatic payments

- Dispute any errors found on reports

Month 2:

- Request credit limit increases on existing cards

- Continue low utilization

- Monitor score improvements

Month 3:

- Consider becoming an authorized user on family member’s card

- Maintain consistent payment patterns

- Evaluate need for secured cards if score is very low

Advanced Credit Optimization Techniques

For serious credit improvement:

- Pay down cards strategically – Focus on cards closest to their limits first

- Use the 15/3 payment method – Pay 15 days before due date, then 3 days before

- Negotiate with creditors – Ask for goodwill removals of late payments

- Consider credit builder loans – Available through credit unions and online lenders

MyFICO – What’s in Your Credit Score

2025 Credit Card Industry Changes You Need to Know

The credit card landscape continues evolving. Here are key changes affecting your credit score:

New Reporting Standards: As of January 2025, some card issuers report balances more frequently, making it crucial to maintain low utilization consistently, not just on statement dates.

Buy Now, Pay Later Impact: Services like Klarna and Afterpay may start affecting credit scores differently. While most don’t report currently, this could change by late 2025.

Inflation’s Effect: With higher costs across everything from Walmart groceries to utility bills, more Americans are carrying balances. Don’t let inflation pressure lead to credit utilization mistakes.

Conclusion: Avoid These Credit Score Killers

These five credit score mistakes – maxing out cards, making late payments, closing old accounts, applying for too many cards, and ignoring report errors – can cost you thousands in higher interest rates and missed opportunities.

The good news? Now you know exactly how to avoid them. Start by checking your credit utilization today, setting up automatic payments, and reviewing your credit reports for errors.

Your future self will thank you when you’re approved for that mortgage, qualify for premium rewards cards, or land that job requiring good credit.

Ready to optimize your credit strategy? Start saving smarter with SmartSaveUSA.com. Check out our guides on maximizing credit card cashback rewards and earning points on Airbnb bookings. For more credit card strategies, explore our complete credit card resource center.